EITC (earned income tax credit) is an important income component for many young frum parents, and especially kollel families. But many don’t understand how the credit is calculated, and often they lose eligibility for it for silly technicalities. All low and middle income families need to be aware of how this government assistance works and how NOT to lose it inadvertently.

Save your savings

For illustration purposes, picture a kollel family that just gave birth to twins. Mazel tov! Of course, they are very excited, but they’re also concerned about how they’d pay their growing bills. Makes sense, right? Their income comes from Mommy’s secretary job and some parental support, which was enough for a family of two, but not the current four. They calculated their future annual expenses, coming out short of about $10,000. It seemed they would need to sell the mutual funds they’d received as a wedding gift, which would cover their estimated $10,000 annual shortfall. It was disappointing to have to dip into their meager savings, yet there seemed to be no alternative. But there is!

Please note: The numbers cited in this article are generally accurate but rounded off for simplicity. Consult a tax professional to discuss your own situation.

Uncle Sam pitches in

This family’s best bet is the EITC, which may bring them over $7,800 annually. Combined with other tax credits, they can almost cover their entire shortfall without touching their modest portfolio. On the other hand, selling their mutual funds is a terrible idea that may lose them the entire EITC! EITC assists working but low-income parents (working singles are eligible too, but for very little) which often includes families headed by students who aren’t yet earning salaries (such as kollel yungeleit).

This government bonus is a significant source of income for married graduate students, but it’s sadly common that young couples inadvertently lose their eligibility, usually by cashing out some small investments. Kollel couples and those who assist them, therefore, need to understand the basics of how the EITC works.

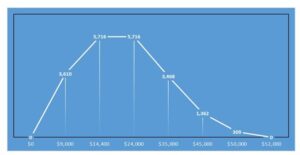

The EITC slide explained

The EITC slide explained

The EITC table follows the shape of a children’s slide, climbing quickly like a ladder, then plateauing onto a small level platform which leads to a gradually declining slide. The credit adds tax refund money to the small salaries of low-income parents, and as the salaries grow above a certain level, the credit is slowly withdrawn. (See chart above. Numbers along the bottom are levels of earned salary income. The numbers along the “slide” are the projected Federal EITC amounts.)

For those with two children, each dollar of work earnings up to $14,400 gets a Federal credit of about 40 cents. (A salary of $1,000 gets $400 from the EITC, a salary of $2,000 gets $800, a salary of $3,000 gets $1,200, etc.) The State than adds in a bonus worth about $2,115, turning a $14,400 salary into a $22,231 take-home pay ($14,400 salary plus $5,716 Federal EITC + $2,115 State EITC). Getting a 52% bonus from the government (Federal + State) adds a lot of incentive for people to raise their incomes, which is good for everyone—the worker, the family, and the economy.

At the top

The 52% bonus is added on the ladder part of the EITC. Then comes the platform: as salary earnings rise from $14,400 to $24,350, nothing is subtracted from the credit. Finally, on the slide portion ($24,350 to approximate $45,000 with one child and $55,000 with 3 or more children), each dollar earned lowers the credit by about 25 cents until it reaches 0.

The platform and gradual slide of benefits help avoid penalizing work, where each extra dollar earned loses so much in credit that people are disincentivized from growing their salaries. Because the EITC encourages working, even conservatives, who are against welfare, tend to be big supporters of the EITC, which has been proven to help families rise out of poverty in a dignified manner.

Falling off the EITC slide

Now, if a young couple decides to sell some mutual funds to unlock some cash, they may be in for a very unpleasant surprise. Because the EITC is designed to help only those with limited means, any couple that earns $3,600 of investment income is disqualified from receiving any EITC for that year. This “unearned income” limit is the same regardless of family size or circumstance (which isn’t really fair), and many a yungerman has learned about this low but strict ceiling the hard way.

Losing $7,831 in EITC (more for those with three children) while pursuing a gain of just $3,600 is bal tashchis of the highest order. It’s especially painful to hear of this kind of loss because there are easy ways to prepare for and avoid this costly error. While the government can be helpful and generous, its tax and program rules are strictly applied, and everyone must follow them to the letter.

EITC + CTC = enough

As long as the depicted family doesn’t sell their mutual funds, disqualifying themselves, tax credits alone will cover most of the $10,000 required by the family at this time. In addition to the EITC, they will receive two Child Tax Credits (CTC). The CTC should provide an additional $1,785 of tax refunds, which combined with the EITC will be almost enough to fill the upcoming gap in the growing family budget ($7,831 EITC + $1,785 CTC = $9,616). For the last few hundred dollars, they can manage on their own!

Tax advice for low-income families

Wealthy people and corporations spend fortunes hiring professionals who maneuver to avoid paying taxes as much as possible (not evading taxes, which is something very different and illegal). As can be seen from the EITC “unearned income” issue, lower-income people have a lot at stake as well in mastering the intricacies of the tax code, but can’t afford to hire teams of experts to guide them. While most frum accountants try to help out those with limited incomes too, there is a limit to how much time they can invest in very small clients. There is no full solution to this problem, though there are various free calculators available, and organizations like LRRC do an excellent job within their limited means.

I thank Yaakov Weiss, CPA, of Weiss Tax & Accounting Services for reviewing this article for accuracy. Tax rules sprawl through dozens of volumes, and everyone needs a professional like Yaakov to help decipher them.

Want to dig deeper?

Try these related articles

Saving Your Earned Income Tax Credit

Taxable Income Shifting: An Easy Way to Lower Tax Bills

Beyond Shevet Levi: Resources to Ease a Difficult Transition